Notable market developments

- Mixed recovered paper prices have decreased in Asia. The apparent easing of supply chain pressures is dragging mixed fibre prices down.

- Australia has a delivered price advantage to Indonesia. An unfamiliar experience for Australian exporters, the proximity to Indonesia means Australian supply is routinely delivered at a lower price than European and North American supply.

Material overview and market summary

Towards the end of August 2022, domestic and international recovered fibre markets maintained their demand strength, with more stable operating environments in Victoria and nationally.

Modest improvements in demand for recovered fibre are being reported in the global supply chain, in part due to Russia’s continuing war on Ukraine. Disruption to global pulp supplies is reportedly sustaining demand for recovered fibre.

Only 2 major grades of recovered paper are traded in any significant volume: old, corrugated cardboard, including those sorted from kerbside collections and the mixed volume derived entirely from kerbside and municipal collections.

Other traditional grades derived from the commercial and industrial (C&I) stream are dwindling as printed media and communications continue to decline. The packaging related C&I materials, including liquid packaging board (LPB) and coated boards, continue to have strong markets, almost entirely for export, underscoring the potential value from increased sorting of these materials, from the kerbside stream.

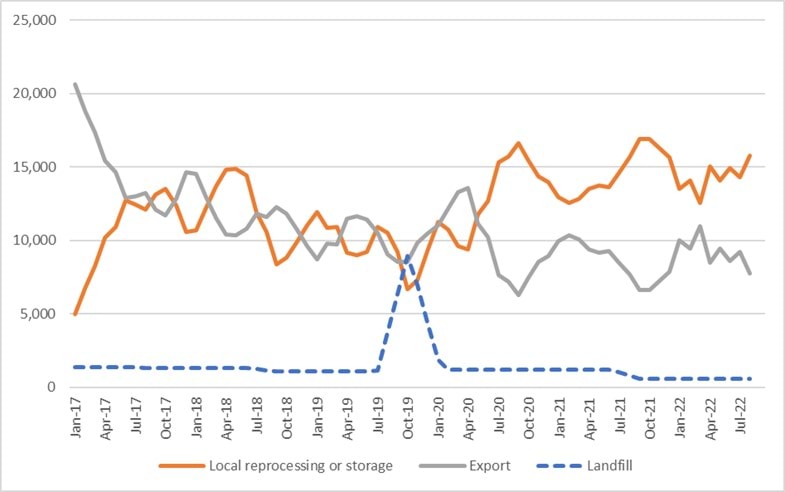

Figure 1: Destination of Victorian material recovery facility (MRF) outputs (tonnes per month) – kerbside paper and paperboard

{kind=link}

Prices, demand and supply

Through to the end of August 2022, global fibre prices remained high, with virgin fibre pulp prices mainly at or near record levels. Virgin wood fibre prices, such as woodchips are in a similar position and consequently, sustaining high recovered fibre prices.

Recovered fibre prices were however moderating towards the end of August 2022 and dropped in September 2022. Asymmetry in global interest rate rises reduced the value of the Australian dollar relative to the main trading currency: US dollars. Some exporters report that they have been able to retain Australian dollar purchase prices, while absorbing the lower US dollar prices on offer.

Demand and supply positions have been little altered over the period to end September 2022. It is expected there will be fewer opportunities to recover fibre from regions of Australia subject to floods and inundation. The impact is reportedly expected to include a modest reduction in exports of kerbside derived recovered fibre from New South Wales and Queensland and is not expected to impact domestic market volumes or prices.

Key end markets and related specifications

There are no new end markets for kerbside recovered paper, despite increased attention on a small number of solutions, from the production of solid board products, to moulded fibre and increasingly, for production of recycled pulp products. Some of these options are relatively small scale and require only limited capital.

The greatest competition in recovered paper markets continues to be for recovered office papers and newsprint, but these are obtained from commercial sources, not kerbside sources. Local paper producers in packaging, recovered paper and tissue products (noting that tissue products cannot go into kerbside collections) and pet care products, all seek office papers and newsprint for different purposes, but the volumes decreased significantly during the pandemic. This market has not recovered and is not anticipated to do so.

Export and interstate market review

As Indonesia has grown its share of the Victorian (and Australian) export volumes, it has brought with it an unfamiliar experience for Australian trade: proximity. A major exporter advised recently they had been able to position their supply into the Indonesian market in part because of the cheaper freight cost compared to North America and Europe.

Recent reports indicate major buyers in Indonesia are aware the Australian Government export licensing provisions for recovered fibre will start in mid-2024 and that the regulations and rules are being considered now. Some buyers continue to describe the Australian laws as a blanket ‘ban’ and advise they intend to seek alternative supply. It seems some of this is fuelled by the commentary of suppliers in other countries.

Just as Australian exporters have an advantage to Indonesia, they have a significant freight disadvantage to India, a market dominated by European and North American suppliers. Although ocean freight rates are decreasing slowly from the peaks earlier in 2022, they are nowhere near as low as they need to be for Australian supply to be competitive into India.

In the meantime, despite volume stability, prices for unsorted or mixed recovered paper fell steeply through the middle of 2022. If the situation continues and prices deteriorate further, gate fees may again become an issue. That applies generally, but the market is aware there are sales of well sorted, low contamination mixed recovered paper for which a premium is still being commanded.

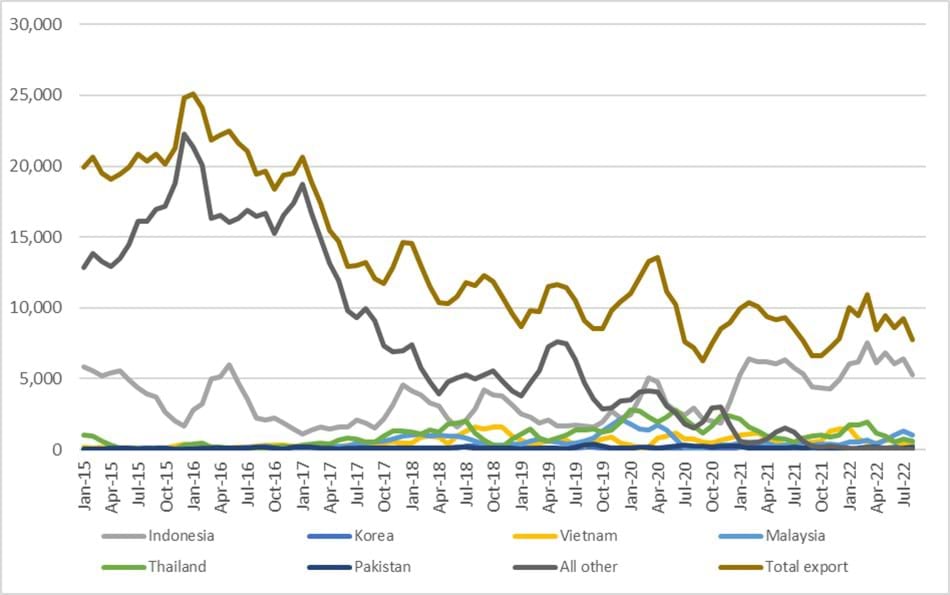

Figure 2: Victorian recovered kerbside paper and paperboard, to export country (tonnes per month)

{kind=link}

Table 1: Annual Victorian recovered kerbside paper and paperboard, to export country (tonnes per year).

| Country* | 2015–16 (tonnes) | 2016–17 (tonnes) | 2017–18 (tonnes) | 2018–19 (tonnes) | 2019–20 (tonnes) | 2020–21 (tonnes) | 2021–22 (tonnes) | 2022–23** (tonnes) |

|---|---|---|---|---|---|---|---|---|

Country* Indonesia | 2015–16 (tonnes) 45,000 | 2016–17 (tonnes) 22,000 | 2017–18 (tonnes) 34,000 | 2018–19 (tonnes) 32,000 | 2019–20 (tonnes) 34,000 | 2020–21 (tonnes) 51,000 | 2021–22 (tonnes) 68,000 | 2022–23** (tonnes) 12,000 |

Country* Korea | 2015–16 (tonnes) 0 | 2016–17 (tonnes) 0 | 2017–18 (tonnes) 1,000 | 2018–19 (tonnes) 1,000 | 2019–20 (tonnes) 1,000 | 2020–21 (tonnes) 1,000 | 2021–22 (tonnes) 0 | 2022–23** (tonnes) 1,000 |

Country* Vietnam | 2015–16 (tonnes) 2,000 | 2016–17 (tonnes) 3,000 | 2017–18 (tonnes) 7,000 | 2018–19 (tonnes) 12,000 | 2019–20 (tonnes) 7,000 | 2020–21 (tonnes) 9,000 | 2021–22 (tonnes) 9,000 | 2022–23** (tonnes) 1,000 |

Country* Malaysia | 2015–16 (tonnes) 1,000 | 2016–17 (tonnes) 2,000 | 2017–18 (tonnes) 10,000 | 2018–19 (tonnes) 6,000 | 2019–20 (tonnes) 16,000 | 2020–21 (tonnes) 4,000 | 2021–22 (tonnes) 6,000 | 2022–23** (tonnes) 2,000 |

Country* Thailand | 2015–16 (tonnes) 2,000 | 2016–17 (tonnes) 4,000 | 2017–18 (tonnes) 14,000 | 2018–19 (tonnes) 11,000 | 2019–20 (tonnes) 24,000 | 2020–21 (tonnes) 19,000 | 2021–22 (tonnes) 13,000 | 2022–23** (tonnes) 1,000 |

Country* Pakistan | 2015–16 (tonnes) 1,000 | 2016–17 (tonnes) 2,000 | 2017–18 (tonnes) 1,000 | 2018–19 (tonnes) 1,000 | 2019–20 (tonnes) 2,000 | 2020–21 (tonnes) 2,000 | 2021–22 (tonnes) 1,000 | 2022–23** (tonnes) 0 |

Country* All other | 2015–16 (tonnes) 214,000 | 2016–17 (tonnes) 184,000 | 2017–18 (tonnes) 81,000 | 2018–19 (tonnes) 67,000 | 2019–20 (tonnes) 45,000 | 2020–21 (tonnes) 18,000 | 2021–22 (tonnes) 3,000 | 2022–23** (tonnes) 0 |

Country* Total | 2015–16 (tonnes) 265,000 | 2016–17 (tonnes) 217,000 | 2017–18 (tonnes) 148,000 | 2018–19 (tonnes) 130,000 | 2019–20 (tonnes) 129,000 | 2020–21 (tonnes) 104,000 | 2021–22 (tonnes) 100,000 | 2022–23** (tonnes) 17,000 |

Source: ABS and IE (Australian Harmonized Export Commodity Classification (AHECC) data by month, classification and destination country, 2022) and Blue Environment.

* Countries ranked by average of last 3 months of exports.

** Partial year across July 2022 to August 2022.

Table 2: Example monthly change in Victorian recovered kerbside paper and paperboard, to export country (tonnes per month).

| Country | July 2022 (tonnes) | August 2022 (tonnes) | Change (%) |

|---|---|---|---|

Country Indonesia | July 2022 (tonnes) 6,400 | August 2022 (tonnes) 5,300 | Change (%) -17% |

Country Thailand | July 2022 (tonnes) 200 | August 2022 (tonnes) 400 | Change (%) 100% |

Country Vietnam | July 2022 (tonnes) 400 | August 2022 (tonnes) 300 | Change (%) -25% |

Country Malaysia | July 2022 (tonnes) 1,300 | August 2022 (tonnes) 1,000 | Change (%) -23% |

Country India | July 2022 (tonnes) 800 | August 2022 (tonnes) 600 | Change (%) -25% |

Country Pakistan | July 2022 (tonnes) 100 | August 2022 (tonnes) 200 | Change (%) 100% |

Country All other | July 2022 (tonnes) 100 | August 2022 (tonnes) 100 | Change (%) 0% |

Country Total | July 2022 (tonnes) 9,300 | August 2022 (tonnes) 7,900 | Change (%) -15% |

Market opportunities

The market continues to expect consolidation that will tighten the recovered paper supply chain. A smaller number of larger market participants increases the prospects for higher levels of domestic recovered fibre processing.

In September 2022, the Victorian Government announced funding support under the Circular Economy Infrastructure Fund. This included a significant activity to recycle LPB of various types, extending to numerous polymer coated packaging formats (e.g. coffee cups).

The recycling process creates a fibre-polymer composite board product, suitable for a range of building and construction activities. This development of saveBOARD products (see https://www.saveboard.nz/ for further details) could result in increased sorting and recycling of the target materials, with the added benefit of improving the quality of the residual mixed recovered paper sorted from kerbside collections.

Report disclaimer

The information on this report was prepared in conjunction with Blue Environment, IndustryEdge and Sustainable Resource Use (SRU).

While reasonable efforts have been made to ensure that the contents of this publication are factually correct, Recycling Victoria gives no warranty regarding its accuracy, completeness, currency or suitability for any particular purpose and to the extent permitted by law, does not accept any liability for loss or damages incurred as a result of placed upon the content of this publication.

This publication is provided on the basis that all persons accessing it undertake responsibility for assessing the relevance and accuracy of its content.

Recycling Victoria does not accept any liability for loss or damage arising from your use of or reliance on the data. The inclusion of information in this report does not constitute Recycling Victoria’s endorsement of any particular facility, or any associated organisation, product or service.

Accessibility disclaimer

The Victorian Government is committed to providing a website that is accessible to the widest possible audience, regardless of technology or ability.

This page contains two embedded complex image files (Figures 1 and 2) that may not meet our minimum WCAG AA Accessibility standards.

If you are unable to read any of the content of this page, you can contact the content owners for an Accessible version.

Contact email: rvdata@delwp.vic.gov.au

Updated