Recycling Victoria market insights reports

Recycling Victoria’s Market Insight Reports provide a snapshot of the waste and resource recovery sector’s market resilience and include:

- market profiles for each kerbside waste stream – paper and paperboard, plastics, glass and metals

- trends and opportunities

- special topics.

The reports combine information from:

- the Australian Bureau of Statistics (ABS) export data and published market reports

- national waste and recycling data

- modelling and insights informed by consultation with industry, government, and community stakeholders.

This report includes export data to the end of March 2023, and pricing updates to the end of April 2023.

If you have any questions, comments or feedback regarding this report or suggestions for future content, please contact Recycling Victoria.

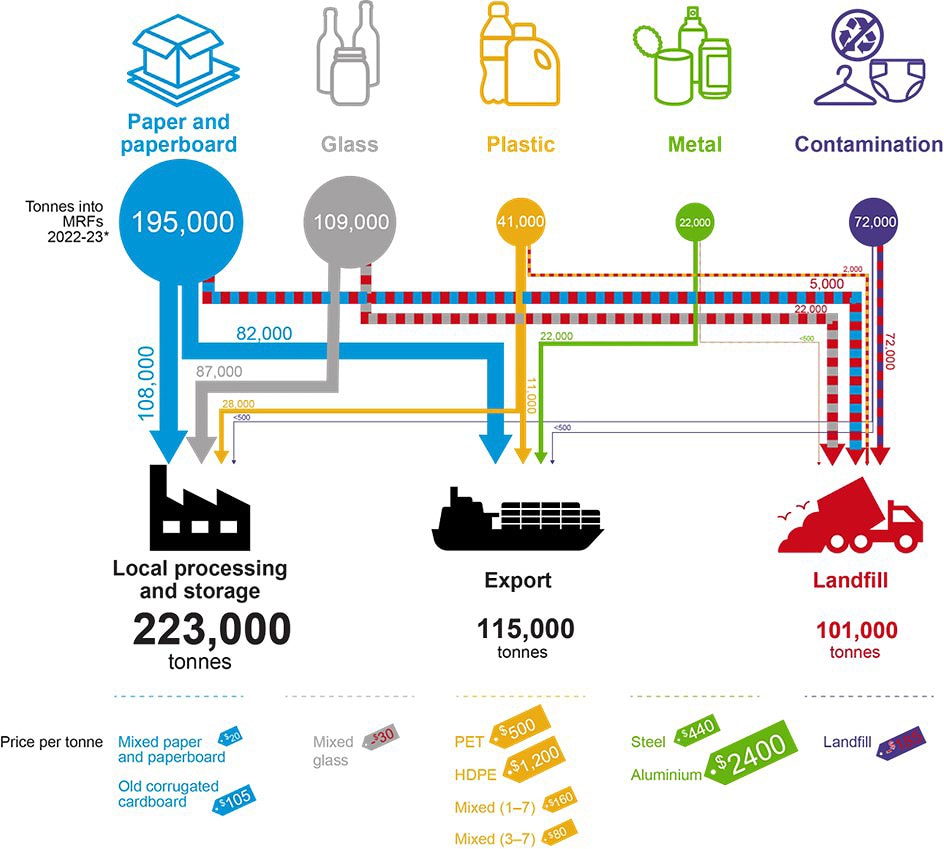

Overview of kerbside recycling bin materials

Figure 1: An overview of the kerbside collected recyclables flow over the 9-month period from July 2022 to March 2023

{kind=link}

Kerbside recycle bin materials sent to landfill

Of the 439,000 tonnes of material collected in the kerbside recycling bin between July 2022 and March 2023:

- 338,000 tonnes (77%) were sent to downstream processing. Of this, 115,000 (34%) tonnes were exported for further processing.

- 101,000 tonnes (23%) were sent to landfill, comprising of:

- 17% contamination removed at material recovery facilities (MRF). This is often non-recyclable material or bagged recyclable material that cannot be sorted for further processing.

- 6% sorting loss at downstream processing facilities, noting that a substantial proportion of this is glass fragments/fines.

The disposal rate to landfill represents an increase of about five percentage points over the long-term average of 17–18%, due to an increase in the reported kerbside contamination rate by councils.

Possible reasons for the increasing contamination rate are included below:

- implementation of the Chinese Operation National Sword policy in March 2018, driving contamination that was previously being left in sorted bales of commodities (in particular paper and cardboard), into the landfill stream.

- improving measurement and sorting of incoming contamination by MRF operators, both following and due to the failure of SKM in July 2019.

- COVID across 2019–20 to 2021–22, resulting in people working at home and generating more waste at home which may have increased contamination in the kerbside recycling bins.

- the public may be putting more in recycle bins thinking that they are doing the right thing but inadvertently introducing more contamination.

- some councils simplifying their messaging for householders, resulting in increased recovery, but also an increased proportion of contamination.

- uptake of fortnightly garbage collections, where households fill up their garbage bins before the two weeks is up and subsequently direct overflow into the organics or recycling bin.

- better contamination data reporting by councils, and changes/improvements in service provider contracts driving improved data reporting.

There are no reports of significant stockpiling by metropolitan MRF operators as of June 2023.

Kerbside materials exported

In March 2023, Victoria’s exports were:

- 29% of national exported post-consumer paper and paperboard (28,400 tonnes of 98,400 tonnes), compared with a 27% average across the 2022 calendar year.

- 64% of national exported post-consumer plastic (2,800 tonnes of 4,300 tonnes), compared with an average 58% across 2022.

The exports outlined above include material sourced through commercial and industrial collections (in addition to municipal kerbside collected materials), and some interstate material, for example from Tasmania. However, the data illustrates the continuing need for additional local remanufacturing capacity and demand in Victoria, particularly with respect to plastics.

This is also the case in the context of the unprocessed scrap plastics export bans which have been phased in over the last 2 years. From 30 June 2021, exports of mixed polymer scrap plastics were banned, which precipitated a 10% drop in the exports of plastics across July 2021–June 2022 (48,000 tonnes) relative to July 2020–June 2021 (53,000 tonnes).

The second (and final) export ban for scrap plastic commenced on 30 June 2022. This again had a significant impact on Victoria, as it is no longer possible to export any recovered plastic packaging that is not sorted into a single polymer type, shredded and washed (without specific export licence exemptions).

Market-wide developments

Paper and paperboard packaging

- Global pulp prices have fallen significantly in the first half of 2023. After reaching all-time highs in the July–December 2022 period, pulp prices fell in line with other commodities, as a result of the global slowdown.

- Mixed recovered paper prices were stable in Asia in the June quarter, but demand remains soft.

- Local market conditions are also under demand-side pressure. Australia’s economic slowdown has begun to flow through to demand for recovered paper.

- Opal Australian Paper’s closure of paper machines at the Maryvale mill has implications for recovered paper demand.

Glass packaging

- CDS Vic is coming into operation in November 2023. Victoria’s container deposit scheme is aiming to be Australia’s most convenient and accessible scheme with more than 600 refund collection points anticipated for the state. VicReturn will be the Scheme Coordinator, and Return-it, TOMRA Cleanaway and Visy will be three Network Operators.

- Visy has expanded its Laverton, Victorian-based beneficiation facility by an additional 100,000 tonnes capacity per year. Visy is expecting to invest in upgrading and increasing the capacity of glass packaging furnaces, including at its Spotswood facility in Melbourne. Visy media statements indicate a target to produce bottles from 60–70% recycled content (up from 30–35% in 2020), with a current recycled content rate of around 45%.

- Increased beneficiation capacity in NSW. ReGroup has commissioned a new glass beneficiation plant in Sydney. This facility is reprocessing some glass packaging from New South Wales that was previously going to Melbourne. This effectively adds beneficiation capacity in Victoria for reprocessing Victorian-generated glass.

- Increased beneficiation capacity in SA. Orora's new glass beneficiation facility in Gawler, South Australia (SA) commenced operations in October 2022. Orora’s new facility will process 100,000–150,000 tonnes per year, helping it reach its target of 60% recycled content in its glass packaging manufacturing by 2025. The facility will mainly target container deposit scheme (CDS) glass from SA, Western Australia (WA) and potentially Victoria once the CDS is in operation from November 2023.

Plastic packaging

- Prices for recovered polyethylene terephthalate (PET) bottles have come off the highs of the middle of 2022 and have been steady across the first quarter of 2023 at around the longer-term average. PET packaging scrap prices have been around $500–$550 per tonne across the January–March 2023 period. Since 1 July 2022, the recycled PET (rPET) must be flaked and washed to be exported, which is putting downward pressure on unprocessed bale prices as local reprocessing capacity catches up with the available local supply.

- Prices for recovered high-density polyethylene (HDPE) bottles have increased across the first quarter of 2023, recovering to a degree from a gradual decline over 2022. HDPE rigid packaging, and in particular natural HPDE (e.g. milk bottles) is highly sought after locally and overseas. Since 1 July 2022, the recycled HDPE (rHDPE) must be flaked and washed to be exported, which could theoretically be putting downward pressure on unprocessed bale prices as local reprocessing capacity catches up with the available local supply. However, prices for rHDPE have remained resilient, reflecting the adequate scale of local reprocessing capacity and many end-market applications for this material.

- In general, many reprocessors reported steady to somewhat increasing prices for reprocessed PET, HDPE and polypropylene (PP) rigid plastic packaging. However, this is against a backdrop of sharply increasing costs. There is benefit in increased local manufacturing to enable local end-markets to match increasing supply, across both packaging and non-packaging plastics recovery.

- Freight costs to overseas market increased significantly in 2022, and while they have fallen markedly, they are still relatively high. Over the last couple of years, the impact of increased freight costs has been exacerbated by increases in export licence fees for reprocessed scrap plastics. In addition, the introduction of the Australian Government's new export licensing rules may have changed end markets for some forms of reprocessed material. Due to local processing costs, export licence fees, and transport costs, local reprocessors may have needed to readjust business models to competitively sell recovered plastics into international markets.

- A number of MRFs and reprocessors reported sending increased quantities of packaging plastics to landfill. This particularly relates to PVC and PS based packaging, and to a lesser extent to lower value grades of PET, HDPE and PP packaging. Over the next few years, this issue should be alleviated by the ongoing phase-out by many brand-owners of PVC and PS packaging, and the redesign of PET, HDPE and PP packaging to improve recyclability and increase the value of the recovered material.

- There is likely to be a market concentration of large-scale PET packaging reprocessors moving forward. From July 2022 export markets were no longer available for unprocessed bales of PET packaging. As a result, the limited number of local reprocessors have greatly increased market purchasing power. There remains a local reprocessing gap for PET packaging until mid-end 2024.

Metal packaging

- Prices for recovered tin-plate steel cans and aluminium beverage cans have recovered strongly over the last three years from the mid-2020 lows. They are trading at relatively high levels, coming off price peaks around March 2022. Prices for both tin-plate steel cans and aluminium beverage cans decreased from the very high prices seen in the first half of 2022 but have been strong and steadily rising across early 2023.

- Exports of tin-plate steel cans and aluminium beverage cans fell steeply from a mid-2021 peak across the 2021–22 financial year but have been rising since mid-2022. The high prices across the 2021–22 financial year probably reduced stockpiles of baled cans built up by material recovery facility (MRF) operators and scrap metal traders during the period of very low prices across the 2020 calendar year. This stockpile drawdown is now complete, and exports have likely stabilised at close to the level of MRF sorting, with the higher prices providing little incentive to stockpile. Exports have trended upwards in 2023 so far, following increasing scrap metal prices.

- Container costs have returned to near pre-COVID-19 levels. International freight costs were very high across the period from mid-2020 to early 2023, putting downward pressure on exports. It is likely that the high freight costs contributed to the high metals price across this period, as exporters had to recoup the container contract cost. Freight costs trended steeply downwards across 2022 and reached near pre-COVID levels by early 2023.

Market opportunities

Market-wide

- Ongoing education program to reduce kerbside contamination. Kerbside contamination appears to be trending up since the pandemic.

- MRF modifications for improved separation (of paper and plastics grades) and contaminant control, supported by improved packaging design and materials selection to reduce incoming low-value or problematic packaging.

- Community recycling drop-off points with a focus on streams such as bulk cardboard.

- Development of industry pathways to provide sufficient skilled workers for the industry. Strong employment growth in the resource recovery sector will be needed.

Fibre

- Large-scale pulping capacity for recovered paper, either separately or integrated with virgin or recycled fibre manufacturing.

- Procurement of locally manufactured recycled products to encourage reprocessing investment.

Glass

- Opportunities associated with the implementation of kerbside glass collection and the container deposit scheme (CDS) collected glass over the next couple of years, coupled with increased recycled content targets.

- Development of export markets for beneficiated glass.

Plastics

- Updated recycled plastics specifications for sorted and reprocessed PET, HDPE, low-density polyethylene (LDPE) and PP from kerbside sources.

- Reprocessing capability for LDPE and PP films from kerbside sources. Preferably into high-quality recycled resin that is competitive with virgin resin and is both useable onshore and exportable.

- Separation equipment for PET/PE/PP at MRF or reprocessing sites for those that currently do not have this.

- Improved packaging design to ensure single and compatible polymer use only, enabling higher recovery rates and less contamination.

Report disclaimer

The information in this report was prepared in conjunction with Blue Environment and IndustryEdge.

While reasonable efforts have been made to ensure that the contents of this publication are factually correct, Recycling Victoria gives no warranty regarding its accuracy, completeness, currency or suitability for any particular purpose and to the extent permitted by law, does not accept any liability for loss or damages incurred as a result of reliance placed upon the content of this publication.

This publication is provided on the basis that all persons accessing it undertake responsibility for assessing the relevance and accuracy of its content.

Recycling Victoria does not accept any liability for loss or damage arising from your use of or reliance on the Data. The inclusion of information in this report does not constitute Recycling Victoria’s endorsement of any particular facility, or any associated organisation, product or service.

Accessibility disclaimer

The Victorian Government is committed to providing a website that is accessible to the widest possible audience, regardless of technology or ability.

This page contains embedded complex image files (Figure 1) that may not meet our minimum WCAG AA Accessibility standards.

If you are unable to read any of the content of this page, you can contact the content owners for an Accessible version.

Contact email: rvdata@delwp.vic.gov.au

Updated